Theoretical Usage

Glossary

Topic

Theoretical Usage: How is it calculated?

Are you wondering how to effectively control costs in your restaurant?

To effectively control costs, it is important to understand theoretical usage in the restaurant industry.

In this article, we will explain what theoretical usage is and how it is calculated, as well as its importance in food cost variance and minimising this to aid restaurant cost control.

What is Theoretical Usage?

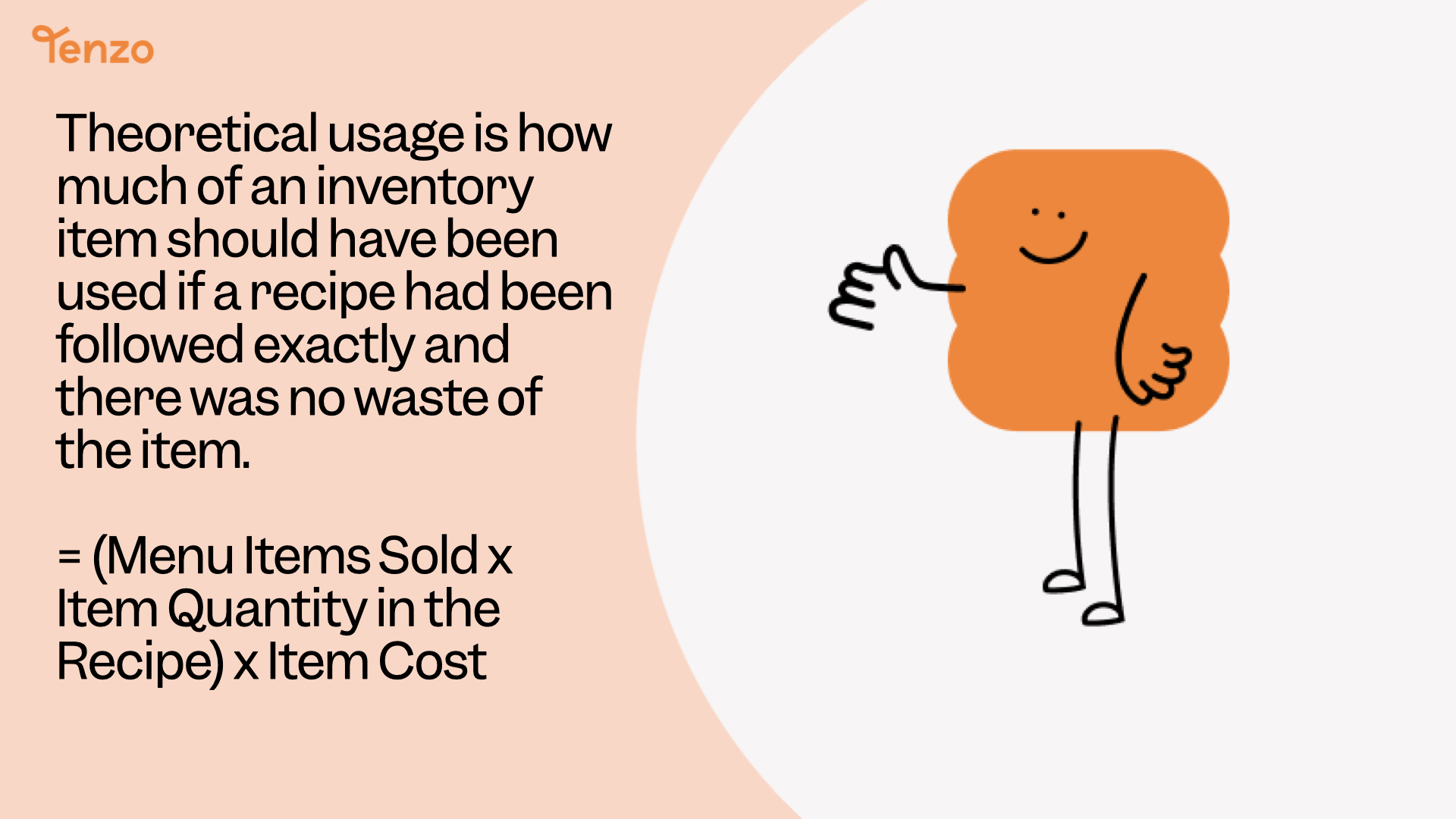

Theoretical usage refers to the calculated amount of ingredients that should be used in a restaurant based on the menu items and recipes.

It is an estimation of the quantity of ingredients that would be consumed if everything was prepared and served perfectly.

Although it’s important to monitor this in the restaurant as a whole, tracking this by menu item helps to identify where the issues are.

Calculating Theoretical Usage

Calculating theoretical usage is fairly straightforward. It involves multiplying the portion size of each ingredient by the number of portions served.

Theoretical Usage = (Menu items sold x item quantity in the recipe) x item cost

This gives an estimate of the total amount of each ingredient that should be used. This calculation takes into account the specific recipes and menu items offered by the restaurant.

Many restaurants now use technology, and inventory management software, to understand their target food costs by calculating theoretical food costs and actual food costs.

Actual vs Theoretical Food Cost

Theoretical food cost is the cost that would be incurred if the ingredients were used exactly as calculated in the theoretical usage. However, as with everything, there are unpredictable events and busy periods that mean the theoretical food cost is not the actual food cost.

Actual food cost, on the other hand, refers to the real cost incurred by the restaurant for the ingredients used. It takes into account factors such as waste, spoilage, and over-portioning.

Actual vs Theoretical means comparing the actual food costs and theoretical food costs, and working out your food cost variance, restaurant owners and managers can identify areas of inefficiency, incorrect operations, and potential restaurant food cost savings.

This involves collecting and analysing data on ingredient usage, portion sizes, and ingredient costs. This data-driven approach allows restaurant owners and managers to identify patterns and trends in ingredient usage and implement food cost control strategies.

Leveraging Theoretical Usage for Cost Control

Theoretical usage can be a powerful tool for cost control in the restaurant industry. Areas of wastage and inefficiency can be identified and this allows them to take targeted actions to reduce costs and improve profitability.

Cost control is of utmost importance in the restaurant industry, where profit margins can be slim. By leveraging theoretical usage, and understanding their food cost variance, restaurant owners and managers can gain insights into ingredient usage and cost that can help them make informed decisions.

This can include adjusting portion sizes, reducing waste through better inventory management, and identifying opportunities for menu optimization. Ultimately, by using theoretical usage as a guide, restaurants can improve their bottom line and achieve greater financial success.

Conclusion

In conclusion, understanding theoretical usage is crucial in the restaurant industry. By calculating theoretical usage, you can accurately track and control food costs, ensuring profitability for your business.

Leveraging this knowledge allows you to make informed decisions and optimise your operations for success. So, take the time to calculate your theoretical food cost and food cost variance to reap the benefits.